Lesson 10

Back to top

Options After High School

Back to top

Teacher Resources

| Resource

| Description

|

| Teacher Resource 10.1

| Key: Academic Acronyms

Make It Local | Modify the list of acronyms to incorporate terms appropriate for your school or community.

|

| Teacher Resource 10.2

| Interactive Presentation Notes and Instructions: Funding Your Education (includes separate PowerPoint file)

Make It Local | Modify two slides in the separate PowerPoint file that compare college costs for students.

|

| Teacher Resource 10.3

| Answer Key: Funding Their Educations

|

| Teacher Resource 10.4

| Assessment Criteria: Options After High School Worksheet

|

| Teacher Resource 10.5

| Key Vocabulary: Options After High School

|

| Teacher Resource 10.6

| Bibliography: Options After High School

|

Teacher Resource 10.1

Back to top

Key: Academic Acronyms

| Make It Local | Modify this document to incorporate acronyms that are appropriate for your community. Make sure that this document and Student Resource 10.1 include the same list of acronyms.

|

Use the following key to help students with their Academic Acronyms list and to facilitate class discussion.

| ACRONYM

| WHAT IT STANDS FOR

| WHAT IT IS

|

| *CAHSEE

| California High School Exit Examination

| A test required by state law to graduate; 10th graders take it in the spring—those who do not pass may retake it in 11th and 12th grades.

|

| *A-G

| Seven different subject areas (a=Social Science, g=Electives, etc.)

| Courses in seven different subject areas needed for graduation and for eligibility to the UC or CSU systems (if completed courses receive C grade or higher).

|

| *GPA

| Grade point average

| An average of points for letter grades earned in a given semester (or cumulatively).

|

| *AP

| Advanced Placement

| Refers to both college level courses offered to high school students and to the standardized subject tests offered each May for possible college credit.

|

| PSAT

| Preliminary Scholastic Aptitude Test

| A practice SAT test given every October; students should take it in their junior year, and it is recommended that they take it in their sophomore year.

|

| SAT

| SAT Reasoning Test

(SAT comes from “Scholastic Aptitude Test,” the former name of this exam.)

| Most colleges require the SAT Reasoning Test (or an equivalent test) for admission. This test has three 800-point sections: Math, Critical Reading, and Writing.

|

| ACT

| The ACT test

(ACT was originally an abbreviation of “American College Testing.”)

| A college admissions test that measures students’ ability to complete college-level work in different subjects. The test covers English, math, reading, science, and writing (optional) and has 36 possible points.

|

| *UC

| University of California

| The UC system is one of California’s public university systems; includes campuses in Berkeley, Davis, Santa Cruz, Los Angeles, and others.

|

| *CSU

| California State University

| The CSU system is one of California’s public university systems; includes SFSU, Humboldt State, Sonoma State, Cal Poly, CSU East Bay, and others. Often referred to as “Cal State.”

|

| CCSF

| City College San Francisco

| A two-year community college in San Francisco; in addition to academic courses, CCSF offers certificate programs in over 100 different career fields, including automotive repair, firefighting, fashion merchandising, multimedia studies, and vocational nursing, among others. Often referred to as “City.”

|

| SFSU

| San Francisco State University

| A public university in San Francisco that is part of the CSU system; often referred to only as “State.”

|

| A.A.

| Associate of Arts, or Associate’s Degree

| A two-year degree offered by many community colleges and career and technical schools.

Some students use the associate’s degree to transfer to four-year colleges or universities.

|

| B.A.

| Bachelor of Arts, or Bachelor’s Degree

| A degree offered by four-year colleges and universities—students receive their degree in specific subject areas or “majors.” If the major is in science, you can earn a B.S., or Bachelor of Science.

|

| M.A.

| Master of Arts, or Master’s Degree

| A graduate degree offered by colleges and universities for one to two more years of course work after the bachelor’s degree. Other examples of master’s degrees include MFA (Master of Fine Arts) and M.S. (Master of Science).

Other examples of graduate degrees that require three to six years of graduate education beyond college include Ph.D. (Doctor of Philosophy, or doctorate), M.D. (Doctor of Medicine), J.D. (Juris Doctor, a law degree).

|

| CHSPE

| California High School Proficiency Examination

| An early-exit exam for California students who are 16–18 years old and have enrolled in the 10th grade for two semesters or more. Equivalent to a high school diploma.

|

| *GED

| General Educational Development

| A national high school equivalency exam that consists of five subject tests. It is not the equivalent of a high school diploma.

|

* Words that students have seen before in this course.

Teacher Resource 10.2

Back to top

Interactive Presentation Notes and Instructions: Funding Your Education

| Make It Local | Modify Slides 3 and 4 of the separate PowerPoint file to reflect college costs for students in your community.

These notes are based on the model version of the presentation. You may wish to modify these notes and update the interactive suggestions accordingly based on your adjustments to the presentation content.

|

1. Before you show this presentation, use the text accompanying each slide to develop presentation notes. Writing the notes yourself enables you to approach the subject matter in a way that is comfortable to you and engaging for your students. Note the ideas for fully engaging the students that are placed at key points in the “Notes” section.

2. Keep in mind that students will continue to work on Student Resource 10.3, Worksheet: Options After High School, during this presentation. Students will also work on Student Resource 10.5, Case Studies: Funding Their Educations, during this presentation.

How much does it cost to go to college? How do people pay for it?

This presentation will answer those questions and help you start thinking about what you can do to prepare to pay for your training or education after high school.

| Presentation notes

Ask students: do you know of any ways that people pay for college? Some students may think that college is only possible for “rich kids” whose parents can pay their entire education. Other students may have a limited familiarity with loans or scholarships.

Reassure students that most college students today do not have their entire bill paid for by their parents and that there are many different ways to fund an education, especially if they start thinking and planning now.

|

You’ve probably heard people talk about how expensive college is, and how people can graduate from college owing thousands of dollars. That makes some people say, “I’ll never be able to go to college!” Don’t give up. College is expensive, but you have a lot of choices about how much you will spend.

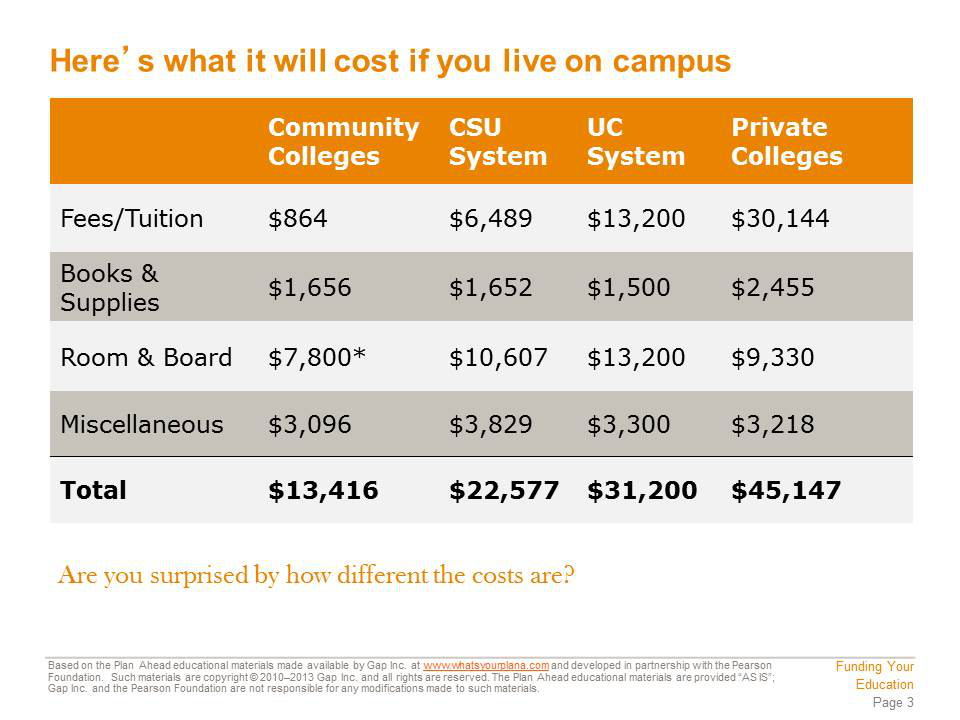

Different colleges have different costs. Community colleges are the least expensive and are great for certificates or associate’s degrees. Plus you can transfer to a four-year college or university. State colleges and universities are more expensive than community colleges, but they offer bachelor’s degrees and graduate degrees. Private colleges and universities also offer bachelor’s and graduate degrees, but they are more expensive than state schools.

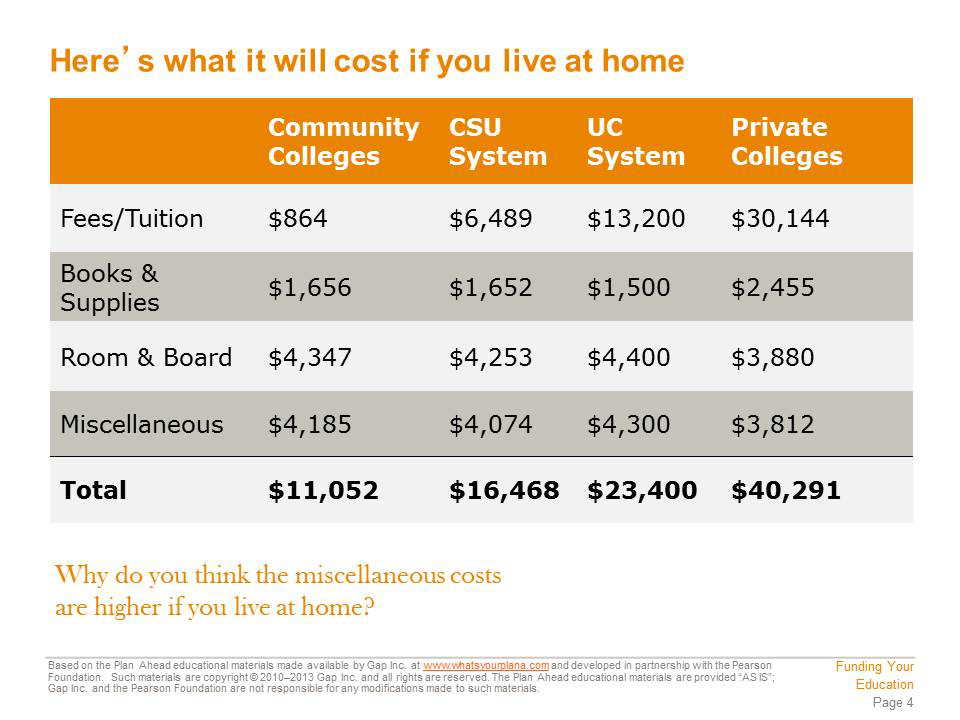

Your expenses will also change depending on where you live while you go to school. If you can live at home while you’re in college, your expenses will be a lot lower than if you live on campus. So if you want to limit your costs, you can go to a community college or nearby state university and continue to live at home while you study. You will be able to get your education, but at a much lower cost.

| Presentation notes

|

These numbers are based on the costs for the 2011–2012 school year. These costs are for a California resident; if someone from outside California wants to attend a CSU or a UC, she will have to pay more money.

Tuition and fees are charged by the college to pay for your classes. Books and supplies include your textbooks and other supplies you will need to do your assignments. Room and board covers your living expenses—paying for a dorm room or on-campus apartment and purchasing a meal plan to eat in the school cafeteria or dining halls. Miscellaneous expenses can include transportation costs, entertainment, and in some cases, health insurance. Many college students continue to use their parents’ health insurance plans, but if you can’t do that, you may be able to purchase a plan from the college.

*This number is starred because most community colleges don’t have on-campus housing.

| Presentation notes

Review the four expense categories on the slide (tuition and fees, books and supplies, room and board, miscellaneous). Ask students to think of examples of these same expenses from their current life. For example:

·

Students may pay additional fees for outside activities.

·

They may have to buy school supplies (pens, pencils, notebooks, etc.).

·

They may bring money to buy food in the cafeteria.

·

They may need money to pay for a bus pass or do fun things with their friends.

Point out that these are all relatively small expenses and that students’ parents may be helping with some or all of them. However, once they graduate from high school, they are adults. If they choose to move out of their parents’ home—whether they will live in a dorm or rent a place of their own—they will have to handle all these expenses on their own.

|

As you can see, your fees, tuition, books, and supplies all cost the same whether you live on campus or live at home. But your room and board costs are a lot lower. You may still want to buy an on-campus meal plan so that you can eat some of your meals on campus between classes, but you won’t be paying for the dorm room or apartment, and you can get a smaller meal plan.

Your miscellaneous costs go up when you live at home, because transportation costs are in the “miscellaneous” category. If you live at home, you will have to commute to school, which means you will need to pay for public transportation or gas if you drive a car. Obviously, your transportation costs will also depend on how close you live to your school. If you can ride your bike or take a short bus ride, your costs will be a lot lower than if you have to drive a car a long way.

Does college still look too expensive? Don’t panic—you can get help paying for your education.

| Presentation notes

Ask students if they can name one nearby school that fits each of the four categories (community college, CSU, UC, and private college or university). Possible answers include:

·

CCSF

·

SFSU

·

Cal State East Bay

·

Sonoma State

·

UC Berkeley

·

UC Davis

·

Stanford

·

USF

·

St. Mary’s

|

Need-based financial aid is distributed to students with financial need.

When you apply to college, you and your family fill out a financial aid form. This form collects a lot of information about how much money your parents make, how much money you make, how many brothers and sisters you have, and so on. This information is used to determine how much need-based financial aid you qualify for.

Merit-based aid is given to students who work hard, get good grades, and are involved in their community. If you’re worried about how to pay for college, work hard in school, get the best grades you can, and do something to make a difference in your community. That will make you a strong candidate for merit-based financial aid. Keep in mind that you can qualify for both need-based and merit-based financial aid, and combining the two types may be your best bet for paying for college.

| Presentation notes

|

Most, but not all, scholarships are merit-based. They may be offered by the school you attend or by private organizations or nonprofit groups. Scholarships are great because you do not have to pay the money back.

There are lots of different scholarships available. Some offer small amounts of money; some scholarships will pay for your entire college education. Getting a scholarship can be very competitive, so it’s a good idea to start researching scholarships early in your high school career. That way you know what you need to do to qualify. Your school counselors can help you find scholarships. You can also visit websites like http://www.fastweb.com

.

Each scholarship has specific criteria you have to meet. You are usually required to have a minimum GPA, and you may also need to demonstrate athletic or artistic talent. Some scholarships are specifically designed for women or for people who represent certain ethnic groups. Others are designed for students who are the first person or first generation in their family to attend college.

| Presentation notes

Ask students to name one specific detail about scholarships. Possible answers include:

·

Scholarships are usually merit-based.

·

You don’t have to pay a scholarship back.

·

Scholarships may be based on what you are going to study in college, on your grades, on your ethnic background, or other factors, like being the first in your family to go to college.

Then ask students: how do you get a scholarship? Answers should include the following steps:

·

Do research on available scholarships (ask a counselor, search online).

·

Meet minimum GPA requirements.

·

Meet other requirements (athletic or artistic achievement, personal characteristics).

Then instruct students to turn to Section 2 of Student Resource 10.3, which is labeled “Complete as you learn more about funding your education.” Ask students to read and answer the first two questions in this section (about need-based and merit-based financial aid).

Tell students to keep the worksheet out, as they will need to do more with it later in this class period.

|

Most grants are need-based and are given by the government or by the college to students who qualify for them – for example, students who meet a minimum GPA requirement. Some grants have different rules; for example, they may expect a student to complete his or her studies within a certain number of years.

| Presentation notes

|

When you borrow money, it’s called a loan, and it must be paid back. You can borrow money from the government or from private institutions like banks. There are lots of different loans available to students who qualify for them.

Obviously, loans are less appealing than scholarships or grants because you have to pay the money back. Many students use a combination of loans, grants, and scholarships to cover the entire cost of their education.

You have already seen how getting a college degree can increase the amount of money you will make in your lifetime. For many people, it is worth it to borrow the money to go to college so that they can increase their earning power later in life. Others prefer not to graduate with debt. Before taking out student loans you should give serious thought to how much debt you feel comfortable taking on.

| Presentation notes

Ask students: what makes a loan different from a grant or a scholarship? Answer: You have to pay it back.

Discuss the question on the slide about why some experts consider student loans to be “good” debt. Ask students: why would owing money for a loan that helped you go to college be seen as better than owing money to help you buy a bunch of new clothes or take a vacation?

Guide students to recognize that borrowing money (for example, by using a credit card) to buy “fun” stuff can be tempting, but you’re setting yourself up to owe money for something temporary. On the other hand, owing money to get a degree is more acceptable to financial experts because it’s seen as an investment in your future. Getting a college degree can help you get a better job, which will put you in better financial position down the road, even if you owe money.

|

Even though $10,000 sounds like a lot of money, it was a good investment in Lakshmi’s future. When she graduates from college, her starting salary is $40,000, which means she will have about $2,000 to spend each month after taxes are taken out of her paycheck.

Student loans are typically offered at lower interest rates, and you will have 10 years to pay them off after you graduate. That means that Lakshmi’s monthly payment is only $100/month. She only spends 5% of her monthly income on her loan, leaving her with $1,900/month to pay for her other expenses. And that’s just in the first year she graduates!

Let’s check back in with Lakshmi a few years later. She’s done well at her job and she has gotten several raises. She now earns $48,000/year, or about $2,800/month after taxes. But she still only pays $100/month for her loan, leaving her with $2,700/month for her other expenses. Plus, Lakshmi now has a good credit history, because she’s been paying her student loan bill regularly. So when she wants to buy a car, she qualifies for a good interest rate.

| Presentation notes

Work through the example on the slide (Lakshmi’s loans and education). Guide students to recognize that even though she borrowed money, after college she ends up in a pretty good financial position. She does have to pay back loans, but she’s making enough that she can pay back the loan pretty easily.

|

Johnny is a hard worker and a good employee, but he still earns less money than Lakshmi does. He has to use his credit card to pay for food and to keep his old, broken down car running, and he builds up credit card debt.

If we check back in with Johnny a few years later, he’s still having a hard time. He’s earned several raises and now brings home about $1,500 every month. He’s got a lot of credit card debt, and his car is getting dangerous to drive. But when Johnny tries to qualify for a loan for a new car, he’s turned down. He doesn’t make much money, he has credit card debt, and he doesn’t have a well-established credit history—all things that a bank will look at when deciding to lend him the money for a car.

In the end, even though Lakshmi borrowed a lot of money, she is doing better financially than Johnny is.

| Presentation notes

Discuss Johnny’s situation with students. Guide them to recognize that while Johnny looks like he’s being smart by avoiding debt, in this case, he’s actually made it harder on himself. Remind students what was discussed a few slides ago about “good debt.”

Then ask students to return to Student Resource 10.3 and answer the third question in Section 2 (on whether or not they would personally take out a student loan). Invite a few volunteers to share their thoughts (if time allows). Students may have different attitudes towards taking out a student loan; do not attempt to tell students their personal opinions are “wrong,” but do make an effort to correct any factual misunderstandings students may have (for example, if they think borrowing the money will hurt their credit rating).

|

Ana had many different options with loans, grants, and scholarships. Since her family doesn’t have a lot of money, she may qualify for need-based financial aid. If her grades are good, she may be able to get scholarships. She can certainly get loans, but she may need those loans to pay for her post-college training.

Ana can live at home to save some money. Another good option s to start getting her education at a community college and then transfer to a four-year school. If it costs $10,000 a year to attend a community college and $20,000 a year to attend a state college, Ana can save a lot of money by going to community college for two years. Look at the totals:

Two years at community college = $20,000 + two years at a state college = $40,000

Total for bachelor’s degree = $60,000

Compare that to four years at a state college = $80,000. That’s a big difference!

Ana could have started saving earlier. Ana used to make money by babysitting. She spent most of that money on clothes and going out. She babysat all through high school. If she’d put $5 each week in savings, she would have had over $1,000 saved up by the time she graduated!

College can be expensive, but it’s worth it. If you start preparing now, you can find ways to pay for it.

| Presentation notes

Review Ana’s situation with students. Help them to recognize that most students will use a combination of these approaches—managing costs, scholarships, grants, loans, etc. —to help them fund their education.

Then distribute Student Resource 10.4, Case Studies: Funding Their Educations. Explain that these scenarios describe real-life situations students might find themselves in as they try to pay for their post-high-school education.

Divide the students into groups of four and assign each group to one of the case studies. Ask them to read the case study and answer the questions.

When students have completed their first case study, form them into new groups. The new groups should have at least one student that worked on each case study (in other words, at least one student who worked on Lorenzo’s story, one who worked on Kanya’s, one who worked on Tai Wei’s, and one who worked on Azucena’s). In these new groups, have students share the basics of their case study and what answers they got. Students should be prepared to answer questions from their group mates.

Then review the answers as a class, using Teacher Resource 10.3, Answer Key: Funding Their Educations. Answer any questions.

|

You can search for scholarships online. Once you know the criteria—the GPA and the other requirements—you can work hard to make sure you are a good candidate for those scholarships.

You can prepare for your SAT and ACT exams. Some scholarships are offered based on those test scores. You don’t need to pay for an expensive test preparation program, and you don’t even need to buy test prep books. The public library has lots of different test prep books you can check out for free. You can also see if you qualify for fee waivers for the tests.

You can take Advanced Placement courses in high school. Not only does that make you more appealing to colleges and scholarship programs, but it can save you money. Some AP exam scores earn college credit, so taking them means you will have fewer courses to take in college.

As soon as you qualify for a work permit, you can get a part-time job and start saving money for college. You might be able to put money aside to pay for your books or to buy a computer to help you do your college homework.

| Presentation notes

|

Take time to talk to your family about your goals for college and ask them to look out for scholarship opportunities for you. Paying for college is a challenge, but it’s an important goal to work towards for your future!

| Presentation notes

|

Teacher Resource 10.3

Back to top

Answer Key: Funding Their Educations

Below are the correct amount responses to the questions about each student’s financing plans.

Lorenzo Brankovic

1. He needs to make $1,473 at his summer job.

2. He will owe his aunt and uncle $5,000.

Kanya Metharom

1. She needs to borrow $1,751

2. She will owe $7,004 after four years.

Tai Wei Guo

1. He needs to borrow $2,900.

2. He will owe $8,700.

Azucena Suárez

1. She needs $6,890 in additional scholarships.

2. If she only receives half of what she needs in scholarships, she will have to borrow $3,445.

Teacher Resource 10.4

Back to top

Assessment Criteria: Options After High School Worksheet

Student Name:______________________________________________________________

Date:_______________________________________________________________________

Using the following criteria, assess whether the student met each one.

| | | Met

| Partially Met

| Didn’t Meet

|

| The assignment identifies two logical post–high-school options for the student, explains thoroughly why those options might be a good fit, and identifies any potential reasons why those options might not work well.

| | □

| □

| □

|

| The assignment demonstrates a good understanding of the criteria for need-based and merit-based financial aid.

| | □

| □

| □

|

| The assignment demonstrates a good understanding of the advantages and disadvantages of taking out a student loan.

| | □

| □

| □

|

| The assignment identifies at least one potential college for the student, explains thoroughly why this option might be a good fit, and identifies any potential reasons why that college might not be a good choice.

| | □

| □

| □

|

| The completed assignment is neat and uses proper spelling and grammar.

| | □

| □

| □

|

Additional Comments:

_____________________________________________________________________________

_____________________________________________________________________________

_____________________________________________________________________________

Teacher Resource 10.5

Back to top

Key Vocabulary: Options After High School

These are terms to be introduced or reinforced in this lesson.

| Term

| Definition

|

| A.A. (Associate’s Degree)

| A two-year postsecondary degree.

|

| ACT

| A college admissions test that measures students’ ability to complete college-level work in different subjects. The test covers English, math, reading, science, and writing (optional) and has 36 possible points.

|

| apprenticeship

| A position at which you learn a specific trade on the job.

|

| art schools

| Postsecondary programs that focus specifically on studio art, design, photography, and other types of visual and performing arts.

|

| B.A. (Bachelor’s Degree)

| An undergraduate degree from a four-year postsecondary program or institution, such as a college or a university.

|

| Cal Grant

| A form of California financial aid for postsecondary education based on both need and GPA that students don’t have to pay back.

|

| career and technical colleges

| Formerly called vocational or trade schools, career and technical colleges offer specialized training to get students into the workforce quickly.

|

| CCSF

| City College of San Francisco, a local community college.

|

| CHSPE

| California High School Proficiency Examination; an early-exit exam for California students who are 16–18 years old and have enrolled in the 10th grade for two semesters or more. Equivalent to a high school diploma.

|

| community colleges

| Also called junior colleges or city colleges, primarily two-year postsecondary institutions that offer certificate and degree (associate’s) programs; can serve as a stepping-stone to four-year colleges and universities. The California Community Colleges System (CCCS) is the largest system of higher education in the world, serving more than 2.9 million students with a wide variety of educational and career goals.

|

| CSU

| California State University; along with UC, one of California’s two four-year university systems. Examples of CSU campuses are SF State, Humboldt State, Chico State, Cal State East Bay, Sonoma State, Cal Poly, and others.

|

| culinary arts

| The art or study of cooking. Students who study or train in the culinary arts may work as chefs, pastry artists, or other related careers.

|

| diploma mill

| Postsecondary institutions that take students’ money without providing substantial education or training.

|

| financial aid

| In this context, money to support one’s postsecondary education.

|

| gap year

| A year off between high school and postsecondary education to gain life experience (and sometimes to earn money) through work, volunteer, or travel.

|

| GED

| General Educational Development; a national high school equivalency exam that consists of five subject tests.

|

| grant

| Need-based college funding given by the government or institution that the student does not have to pay back.

|

| major

| Discipline or subject area of focus for an undergraduate degree.

|

| online program

| A postsecondary program at which one studies online by attending “virtual courses” on the Internet rather than a physical campus.

|

| PLAN

| The (optional) practice ACT exam taken in the 10th grade.

|

| PSAT

| The practice SAT Reasoning Test taken in the 10th and 11th grades.

|

| SAT

| The SAT Reasoning Test; a college admissions test that has three 800-point sections: Math, Critical Reading, and Writing.

|

| scholarship

| Assistance for education based on merit and/or financial need.

|

| student loan

| Private or federal funds qualified students may borrow for postsecondary education and repay upon graduation.

|

| UC

| University of California ; one of California’s public university systems—with undergraduate campuses in Berkeley, Davis, Santa Cruz, Los Angeles, and six other locations.

|

Teacher Resource 10.6

Back to top

Bibliography: Options After High School

The following sources were used in the preparation of this lesson and may be useful for your reference or as classroom resources. We check and update the URLs annually to ensure that they continue to be useful.

Back to top

Print

Getting Ready for Life After High School, 2009-2010. Los Angeles: Los Angeles County Office of Education, 2009.

High School-College-Career Handbook, 2007-2008. San Francisco: San Francisco Unified School District Pupil Services Department, 2007.

Lapan, Richard T. Career Development Across the K-16 Years. Alexandria, VA: American Counseling Association, 2004.

Noonan, Shannon. “College Knowledge: College 101.” PowerPoint presentation, UC San Francisco CSEO/EAOP, 2010.

Back to top

Online

“About Your Higher Education—Options in California.” CaliforniaColleges.edu,

http://www.californiacolleges.edu/explore-colleges/about-your-higher-education-options-in-california.asp

(accessed July 2, 2012).

“AmeriCorps.” Wikipedia,

http://en.wikipedia.org/wiki/AmeriCorps

(accessed July 2, 2012).

“California Community Colleges System.” Wikipedia,

http://en.wikipedia.org/wiki/California_Community_Colleges_System

(accessed July 2, 2012).

“California State University.” Wikipedia,

http://en.wikipedia.org/wiki/California_State_University

(accessed July 2, 2012).

“Community Colleges.” California Community Colleges Chancellor’s Office,

http://www.cccco.edu/CommunityColleges/tabid/830/Default.aspx

(accessed July 2, 2012).

Hansen, Randall, Ph.D. “Next Step After High School? Some Alternatives to College.” Quintessential Careers,

http://www.quintcareers.com/college_alternatives.html

(accessed July 2, 2012).

“How Much Does College Cost?” CaliforniaColleges.edu,

http://www.californiacolleges.edu/finance/how-much-does-college-cost.asp

(accessed July 2, 2012).

Littlefield, Jamie. “Types of Financial Aid.” About.com,

http://distancelearn.about.com/od/payingforschool/a/typesofaid.htm

(accessed July 2, 2012).

“Sample Financing Plans.” CaliforniaColleges.edu,

http://www.californiacolleges.edu/finance/sample-financing-plans/sample-financing-plans.asp

(accessed July 2, 2012).

“University of California.” Wikipedia,

http://en.wikipedia.org/wiki/University_of_California

(accessed July 2, 2012).

“What Are PLAN, PSAT, ACT and SAT.” Summit Academy,

http://www.summit-academy.com/HighSchool/educational%20planning/Docs/College_Preparation_Tests.pdf

(accessed July 2, 2012).

Back to top

Based on the Plan Ahead educational materials made available by Gap Inc. at

www.whatsyourplana.com

and developed in partnership with the Pearson Foundation. Such materials are copyright © 2010–2013 Gap Inc. and all rights are reserved. The Plan Ahead educational materials are provided “AS IS”; Gap Inc. and the Pearson Foundation are not responsible for any modifications made to such materials.