Lesson 8

Personal Finance

Teacher Resources

| Resource | Description |

| Teacher Resource 8.1 | Guide: Guess the Cost Game

Make It Local | Modify this section for your community. Updates require researching current economic information. |

| Teacher Resource 8.2 | Interactive Presentation Notes and Instructions: On Banking (includes separate PowerPoint file) |

| Teacher Resource 8.3 | Flash Cards: Banking (separate Word file) |

| Teacher Resource 8.4 | Key: Flash Cards on Banking |

| Teacher Resource 8.5 | Test: Banking |

| Teacher Resource 8.6 | Answer Key: Test on Banking |

| Teacher Resource 8.7 | Key Vocabulary: Personal Finance |

| Teacher Resource 8.8 | Bibliography: Personal Finance |

Teacher Resource 8.1

Guide: Guess the Cost Game

| Make It Local | Research average estimated monthly expenses for a single adult living in your local community. Below are example expenses for a single person living in San Francisco as of June 2012. Prepare small poster boards using these expense categories and the accompanying images, or replace the categories and images with ones more appropriate for your local community. Write the cost of each expense on the back of the board so students cannot see it. Once you have identified the costs you plan to use, modify Student Resource 8.1 to match the expenses and categories you used. |

Studio (One Room) Apartment: Mission District

$1,635

One-Bedroom Apartment: North Beach

$2,340

One Bedroom in Shared Three-Bedroom Apartment w/ Two Roommates: Marina

$1,210

Car Payment: Used 2009 Toyota Prius

$264

SFMTA/MUNI: Adult Monthly Pass (includes BART)

$74

Cell Phone Plan: iPhone with Unlimited Voice and Texting

$140

Telephone Plan: Home Phone/Landline

$30

Household Utilities: Electric

$58

Household Utilities: Natural Gas

$55

Groceries: Per Person

$254

Teacher Resource 8.2

Interactive Presentation Notes and Instructions: On Banking

Before you show this presentation, use the text accompanying each slide to develop presentation notes. Writing the notes yourself enables you to approach the subject matter in a way that is comfortable to you and engaging for your students. Note the ideas for fully engaging the students that are placed at key points in the “Notes” section.

This presentation will teach you about banks and credit unions—how they work and why they are a good place to keep your money. | Presentation notes

Before you show the presentation, let students know that there will be a test on the information presented later in the lesson so they should pay close attention. |

There are two main kinds of bank accounts: savings and checking. You can deposit your paycheck into your checking account, and that money is available to you for paying your bills. You also use this account to withdraw cash. The money that you don’t want to use for everyday expenses is kept in a savings account. You can take a little bit of your paycheck and put it into your savings account. This money will accumulate and be available for something really important that you want to pay for in the future, like going to college or buying a car. Putting money into your bank account is called making a deposit. Taking money out of your account is called making a withdrawal. You can make deposits and withdrawals by going to the bank or by using online banking services. Many people have something called direct deposit. Their paychecks go straight into their checking accounts, and they don’t have to go to the bank to deposit them. | Presentation notes

Post the following terms/phrases on the board: · Savings account · Checking account · Making a deposit · Making a withdrawal · Direct deposit Point out that students have seen some of these terms before in the “I Need to Stop at the Bank” reading. Call on a volunteer to explain or define one of the terms. Repeat the process until all terms are defined and clear up any misunderstandings. |

Banks and credit unions offer the same services. But there are a few big differences. Banks are for profit: they are owned by investors who want to make money. Credit unions are not for profit and they are owned by their members. So if you keep your money in a credit union, you are a partial owner! Since a credit union isn’t trying to make a profit for its investors, it can offer lower fees and lower interest rates for people who take out loans. Then why doesn’t everyone join a credit union? Many credit unions are designed to serve a specific group of people—such as union employees, students, or teachers. Some credit unions serve people who live in a specific neighborhood. So you have to check and see if you qualify for membership in a credit union. Also, they may not be as convenient as banks. Credit unions are usually located in just one building, but banks can have many branches, or local offices, so you can take care of bank business even if you aren’t near one specific branch. Both banks and credit unions offer online banking services so that you can manage your finances no matter where you are. | Presentation notes

Draw a Venn Diagram or other compare/contrast chart on the board (or project one using a Promethean Board). Have students compare and contrast a bank and a credit union, based on the content and notes from this slide. Specifics about Banks: · Banks are for profit. They are owned by investors. · Banks serve anybody. · Banks often have lots of branches. Specifics about Credit Unions: · They are nonprofit. They are owned by their members. · Credit unions may only serve a specific group of people, like people who do a certain job or live in a certain neighborhood. · Credit unions may only have one location. About Both: · They are reliable, safe places to put your money. · They offer similar services— checking accounts, savings accounts, loans, etc. · They usually offer online banking. |

Some people who are not US citizens or who are undocumented are afraid to use banks. Some people don’t want anyone to know how much money they have. But you don’t need to worry about any of that with banks. US banks have confidentiality rules, which means they have to keep your information private. Some banks encourage undocumented workers to open bank accounts. People who come from countries where it is more common to deal in cash may avoid banks in favor of keeping their money at home. They are not sure if they can trust banks. We’ve been hearing stories about banks “failing,” but this doesn’t mean that people have lost their money. All US banks and credit unions have insured deposits. In the United States, any money you put in a bank is insured up to $250,000, thanks to the FDIC, or Federal Deposit Insurance Corporation. The FDIC was created by the US government after the Great Depression, when lots of people lost money because banks made bad investment decisions. Today, even if a bank fails, the FDIC will pay you back, so you don’t need to worry about losing your money if you put it in a bank. Credit unions are also insured through the National Credit Union Administration. | Presentation notes

After students read this slide, ask them: what is one reason why people are reluctant to put their money in a bank or credit union? The most common answers should be: · Because undocumented immigrants are scared to use a bank · Because they don’t want people to know how much money they have · Because they’re afraid they’ll lose their money if the bank fails Then point out that these fears are based on people not fully understanding how a bank works. Ask students: what could you say to someone who has one of these concerns? The answers should be: · Some banks specifically offer services for undocumented workers. · Banks have strict rules about confidentiality, so they can’t tell people how much money you have or share other personal details about you. · Bank accounts are insured through the FDIC, so if you have an account up to $250,000, you will get your money back, even if the bank fails. Credit unions are also insured. |

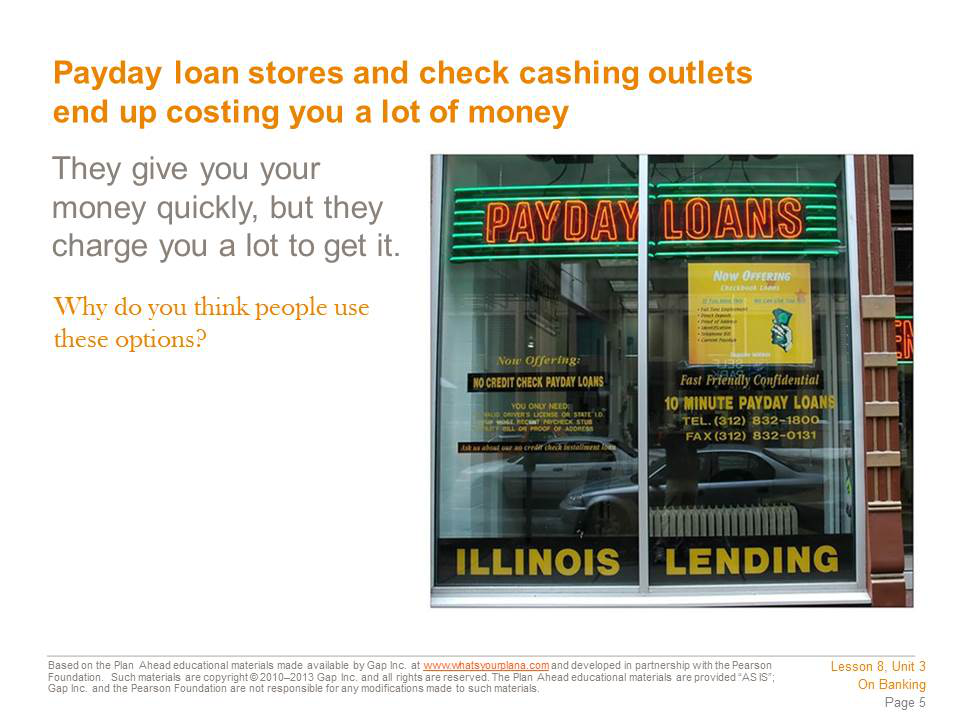

Many people use payday loan stores or check cashing outlets to get access to their money without using a bank. But this is not a good idea. Payday loan stores will advance you money on your upcoming paycheck. Imagine that you will get paid next week and you know your check will be $200. But you need that money this week to pay your bills. A payday loan store will give you the money this week, but they will charge you for the money they are lending you. So you might have to pay $30 to get that $200 early. If you kept your money in a bank, you wouldn’t pay anything to get access to your money. It’s true that banks can’t give you your paycheck money early, but they can help you with good budgeting and money management. Some institutions offer ways to help people stop using payday loans (as well as build their credit ratings, which you will learn about later). Check cashing outlets are another way people avoid using a bank. You can take your paycheck to one of these places and they will give you the amount of the check in cash. So what’s the problem? They may charge you 2–3% of the amount just for having the check cashed. Again, you are paying someone to get access to your own money. And unlike a bank or a credit union, you won’t earn interest. Still, a lot of people use these options instead of banks and credit unions. They are called unbanked or underbanked. | Presentation notes

Ask students: what does it mean when someone is “unbanked” or “underbanked”? Invite students to discuss the question on the slide. Guide students to recognize that people using payday loan or check cashing stores may not realize how using these services can make it harder for them to save money and improve their financial circumstances. |

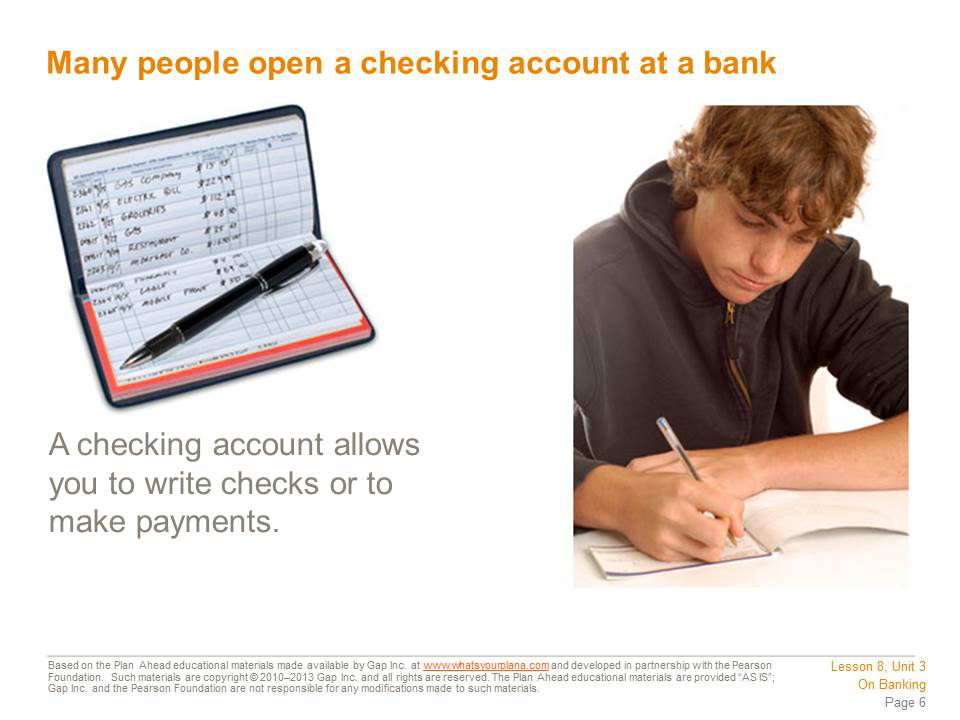

Most people use their checking account as a way to pay their expenses. Let’s say you have graduated from college. You’re working full-time and sharing an apartment with some friends. You will have certain expenses to pay for: your rent, your utilities, your food, maybe a cell phone bill, and maybe a payment on a student loan. You need a way to pay these expenses, so you open a checking account and keep your money in it. Now you can write a check to your landlord for the rent, write a check to pay your student loan bill, and so on. When the landlord receives your rent check, he deposits it into his bank account, and your bank transfers that amount out of your account and into his account. When people say the check “cleared,” they mean this process occurred successfully. So long as you have money in your account to cover the amount of your check, the check will clear. | Presentation notes

|

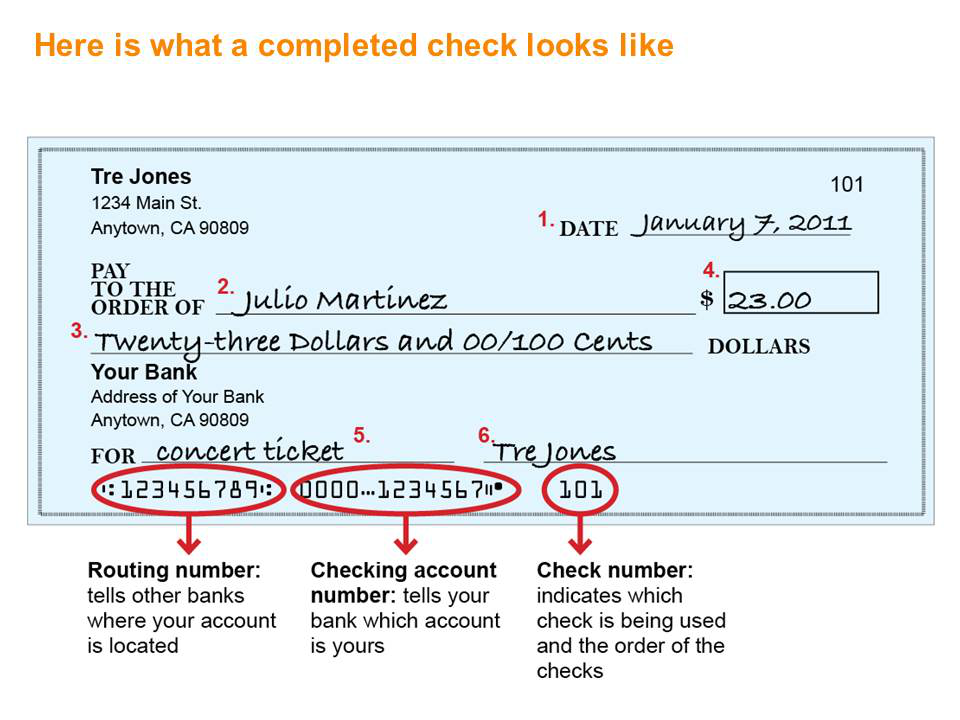

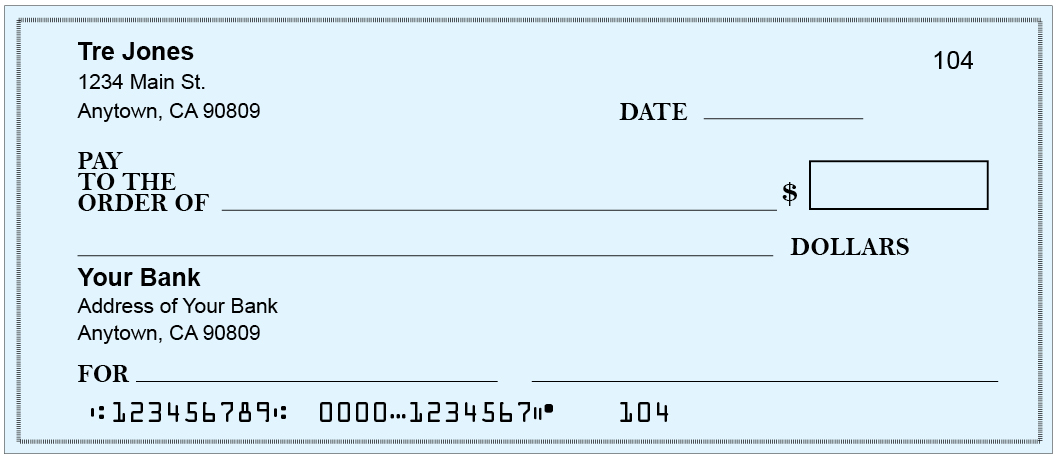

After talking with Julio, Tre decided to open a checking account. Once he received his first checks, he decided to write one for $23 to Julio to pay him back for a concert ticket. These are the steps he followed to write his first check: 1. Enter the date in the upper right-hand corner. Include the month, day, and year. 2. Write the name of the person or business that you are making the check to on the Pay to the Order of line. If it’s to a person, write the first and last name. 3. Write the amount of the check in word form. 4. Write the amount in number form next to the dollar sign, including dollars and cents. 5. Include any information you’d like on the memo line, such as what you’re paying for. 6. Sign your check; it can’t be cashed or deposited into an account without your signature. Keep in mind that it needs to be your complete signature. Your bank will have a copy of your signature on file, so don’t sign with a nickname or with just your first name. You need to sign every check with your full name; some people even use a middle name or middle initial on their checks. | Presentation notes

Review this slide with students, walking them through every element that goes on a completed check. Then distribute Student Resource 8.6, Guided Practice: Managing a Checking Account. Ask students to read and complete the first section (A Check for the Utilities). After students have completed the practice check, review it as a class and answer any questions. |

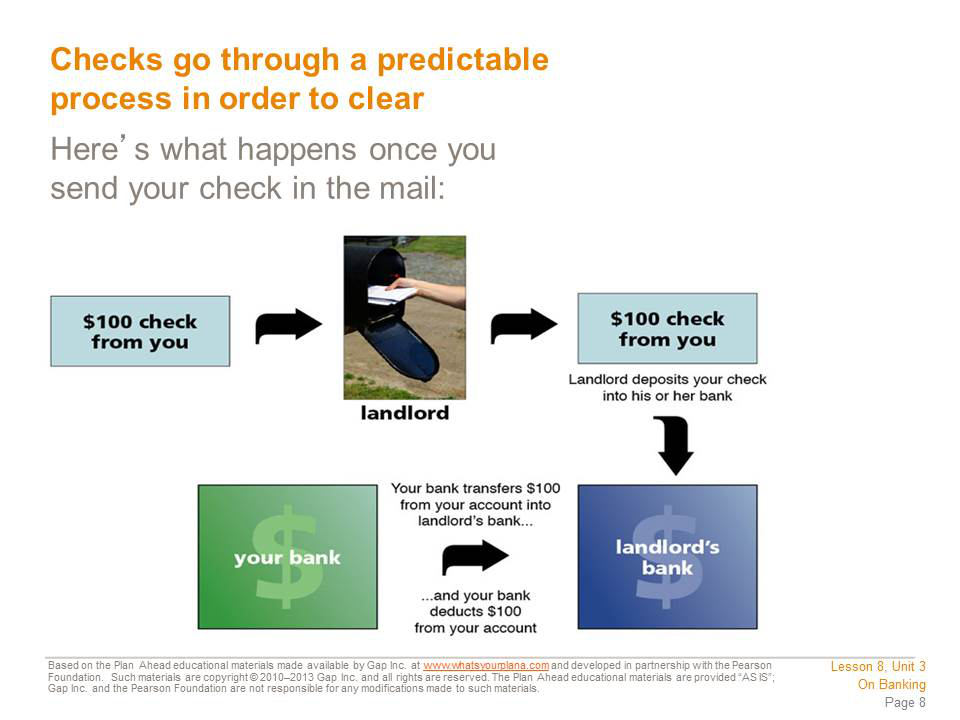

It can be hard to imagine how money comes and goes from your account when you write a check, but it’s pretty straightforward. In this example, the check is to the landlord. Once the landlord deposits your check into her account, her bank immediately contacts your bank with the amount to be transferred. Both of your banks keep accurate records of the whole transaction: the number of the check and the amount it was for, exactly what day the money was transferred out of your account and into the landlord’s, and what each of your account balances are now. The information about your account will appear on your monthly statement. This check clearing process may soon be a thing of the past. These days checks are becoming less common as more and more people are using online banking services to pay their bills. We’ll talk more about online banking later. | Presentation notes

|

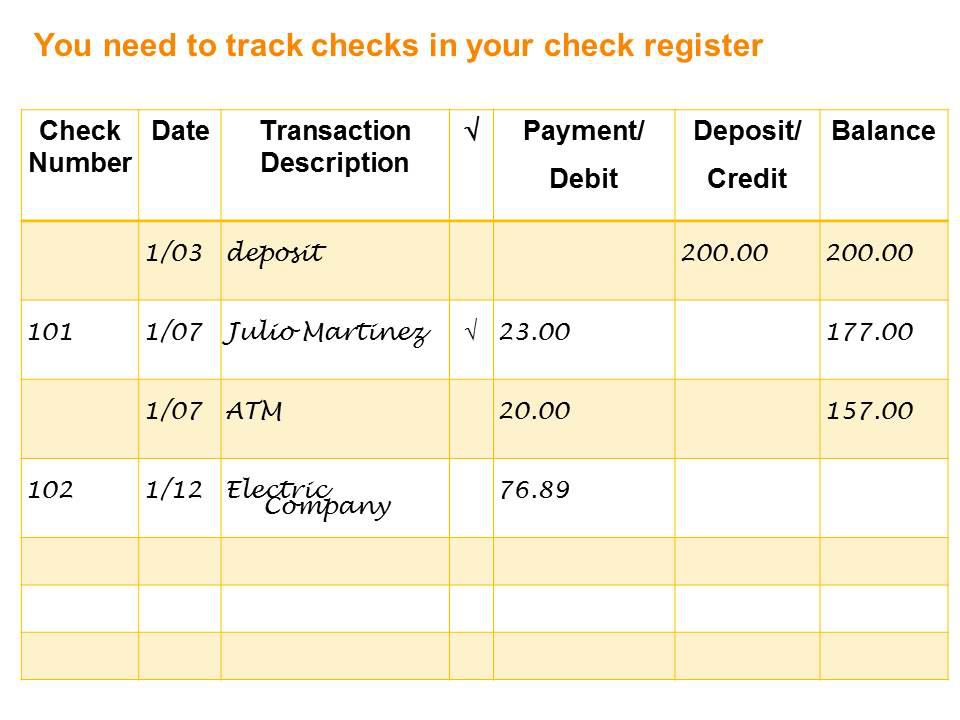

Each box of checks comes with a register, a booklet you use to keep track of payments, purchases, and deposits. Each time Tre uses money from his account—whether by check, debit card, or ATM withdrawal—or makes deposits, he updates the register like this: 1. Writes the check number from the upper right-hand corner of his check. 2. Writes the date he wrote the check. 3. Writes who he wrote the check to in the Transaction Description column. 4. Writes the amount of the check in the Payment/Debit column. 5. Uses the Deposit/Credit column when he puts money into the account. 6. Writes the new total in the Balance column each time he debits or credits his account. 7. Every time a check clears, he puts a check mark next to it in his register. | Presentation notes

Review this slide with students, making sure they understand how to make an entry in a check register. Then ask students to complete the next section (Tre Manages His Check Register) of Student Resource 8.6. When students have finished, discuss their answers and answer any questions.

|

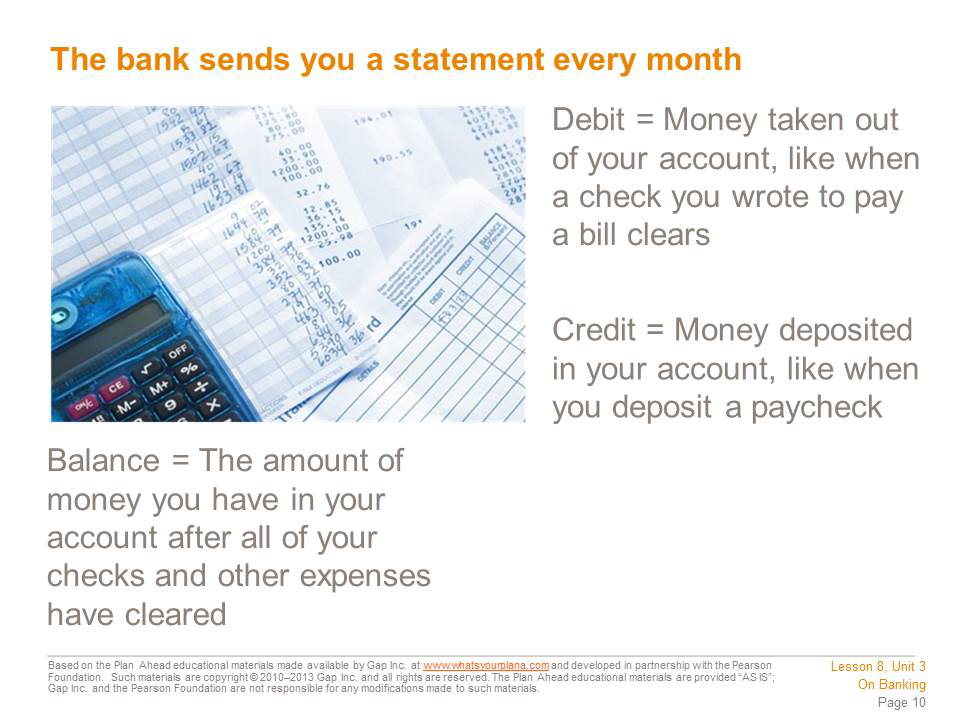

Every month your bank sends you something called a statement. It lists all of the banking activity that occurred in the previous month, including which checks cleared. You should compare your check register to your monthly statement. That way you know which checks have cleared and which ones are still outstanding—meaning that they haven’t been withdrawn from your account yet. Comparing your own records with the bank statement is called balancing your checkbook, and it will help you keep track of your money. | Presentation notes

|

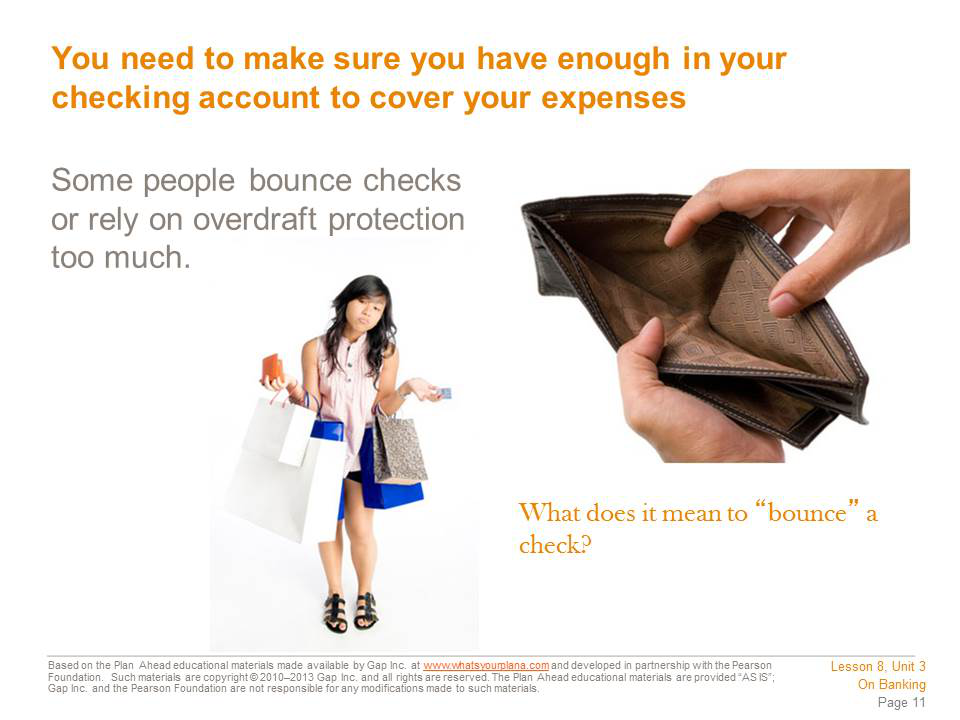

If you write checks that you can’t pay, the checks will “bounce,” or be rejected by the bank. Imagine you have spent all the money in your account, but you see something that you really want to buy. You can write a check, but when it goes to the bank, you won’t have the money to pay for it. So your check will be rejected—it will bounce. Banks will charge you a fee if you bounce checks, and if you bounce a lot of checks, you can get in trouble with the law. Some stores don’t take checks because too many customers’ checks have bounced. Some banks offer overdraft protection, which helps to ensure that you will never bounce a check. If you have overdraft protection on your account and you write a check you can’t pay for, the bank will loan you enough money to cover the check. But once you have money in your account again, the bank will take its money back and charge you a fee. The bank can also transfer money out of your savings account into your checking account to cover the amount, if you have that money available in a savings account. But you still have to pay a fee. | Presentation notes

After students read the slide, discuss the concept of overdraft protection. Ask students: what are the pros and cons (good points and bad points) of having overdraft protection on your checking account? Provide an example: You know you’ll get paid next week, so when you see something on sale for $25, you write a check for it, even though you know you don’t have money in your account right now. The check gets to the bank. The bank sees that you don’t have $25 in your account, but you do have overdraft protection. So the bank pays that check for $25. A week later, you get your paycheck and deposit it in the bank. The bank sees that you have money now, so they take out the $25 you owe them for that check. However, the bank doesn’t want you to use overdraft protection, so they might charge you an additional $15 in fees, just to remind you to only spend what you actually have. Guide students to recognize that having overdraft protection on your account can be a good thing, because you don’t want to bounce a check. If you bounce a check, you can get in trouble with the person or company you wrote the check to—and that could be really bad if you bounce a check for your rent or your car payment. You could get evicted, for example, or the car company could repossess your car. However, you should try to be careful and avoid using your overdraft protection, because any time you use it, your bank will charge you a fee, so you’re losing money. It will also damage your credit history. Explain this concept briefly and let students know that they will learn more about it later in the course. |

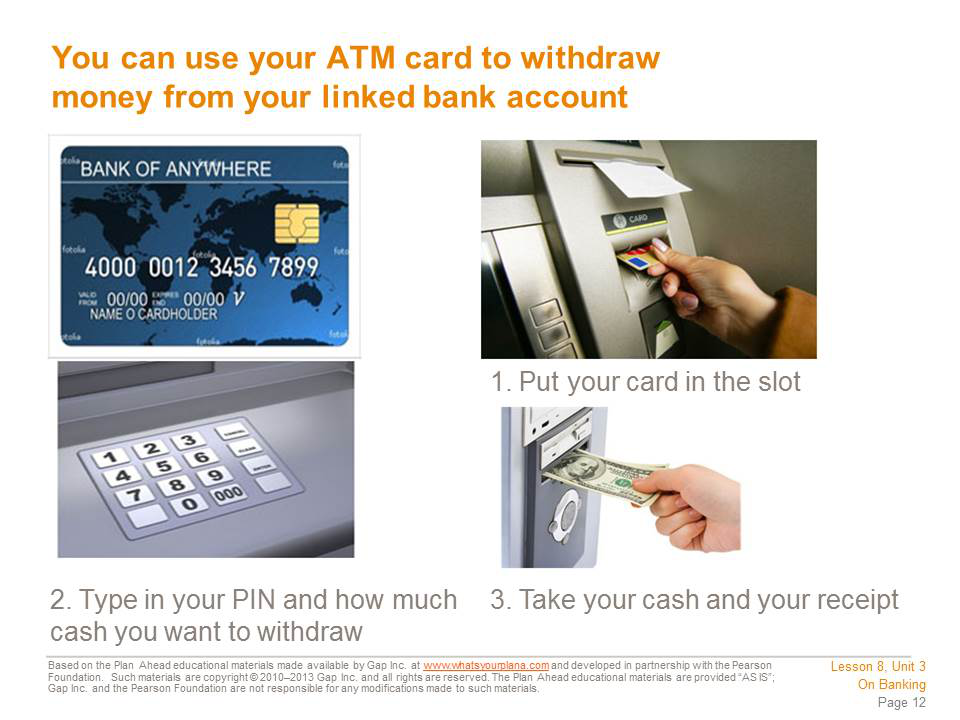

An ATM (Automated Teller Machine) is a machine that gives you access to your money even if the bank is closed. ATMs are often outside of bank branches, but they can be many other places as well. ATMs are part of a network, sort of like a computer network, so even if you keep your money in Bank of America, you can use an ATM at a Wells Fargo Bank and still get your money. However, if you use an ATM that isn’t part of your bank network, you may be charged a fee. To access money at an ATM, you need an ATM or a debit card. You insert the card into the machine and then enter a PIN, or personal identification number. Your PIN is a way of proving to the machine that you really are the person who is supposed to have access to this account. You punch in the amount you want to withdraw, and that amount comes out of the money slot. | Presentation notes

Ask students if they have ever used an ATM or have ever seen a parent or a friend use an ATM. If they have, ask them: what other things can you do at your bank’s ATM? Possible answers include: deposit a check, check your account balance, and even buy stamps. If students have not seen someone use an ATM, you may wish to physically act out the steps of using an ATM or have a student or students act it out.

|

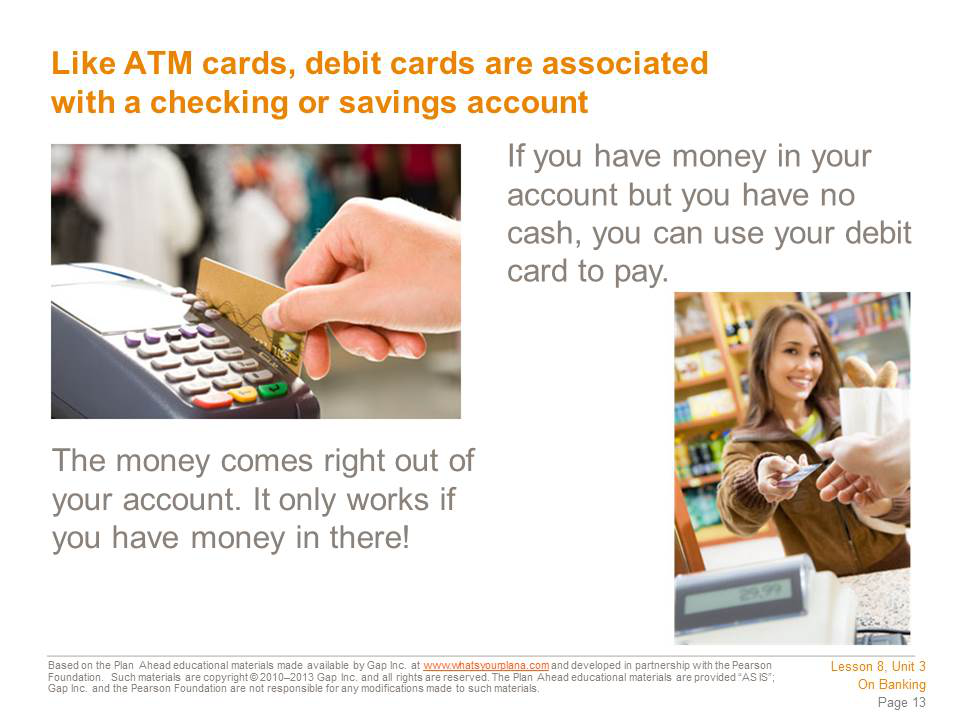

Debit cards are also very popular nowadays. A debit card is an ATM card that can be used to make purchases. If you want to get gas for your car or buy groceries, you can “swipe” your debit card rather than write a check or pay cash. However, when you use your debit card, it takes money right out of your checking account, just like writing a check. You need to track your debit card purchases just like tracking your checks, so you always know how much money you have left in your account. Debit cards look like credit cards. But a credit card doesn’t take money out of your account. Instead, using a credit card is like borrowing money from a bank, which means you will have to pay it back. If you hear a cashier asking a customer “debit or credit?” it means they need to know whether the purchase will be coming from a person’s bank account or charged to her credit card. | Presentation notes

Ask students: how is a debit card similar to/different from a credit card? Possible answers include: · Both cards allow you to buy things without carrying cash in your wallet; however, debit cards draw money directly out of your account, while a credit card borrows money from a bank, which you will have to pay back with interest. · Credit cards can get you into financial trouble, because you can borrow a lot of money and then you need to pay it all back. Debit cards are safer, because you’re using your own money, but you need to pay attention and track your purchases just like you would track a check that you write.

|

Banks pay interest because they get to use your money. If you put in $100, the bank takes that money and uses it. How do banks use your money? They lend it to other people. The bank takes your $100 and the money that other people have put in the bank. It lends this money to other people so they can buy a car or a house or open a business. The bank makes money on that loan, so it gives a little bit of what it earns back to you. The interest the bank pays you is an incentive for you to invest your money at its institution.

| Presentation notes

|

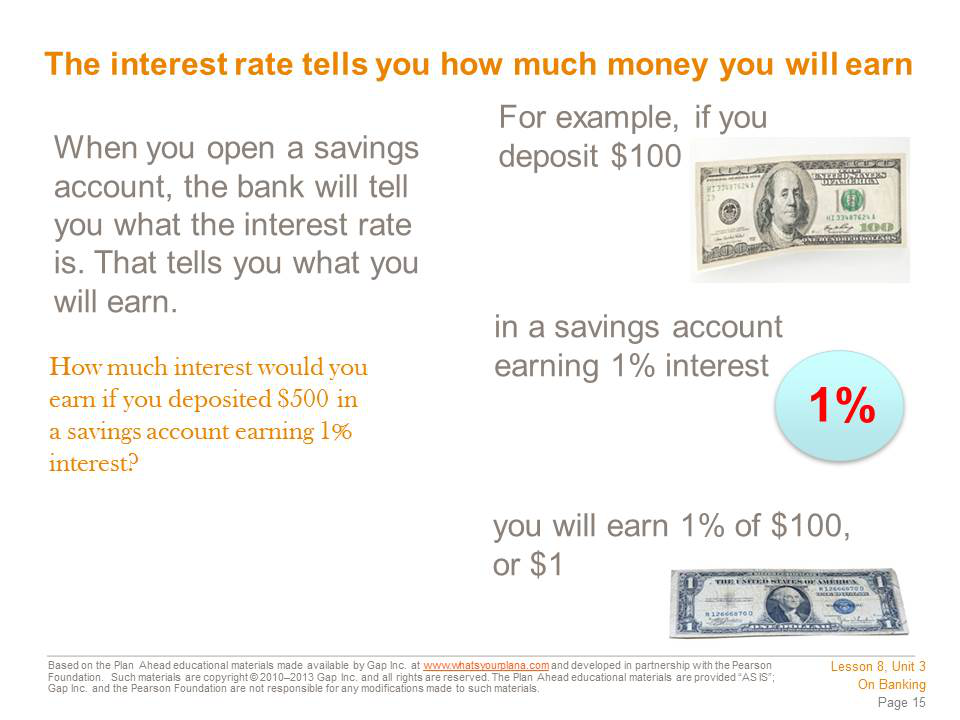

There are many different types of savings accounts and each type offers a different annual, or yearly, interest rate. If you had $500 and you deposited it in a savings account earning 1% interest annually, you would earn an additional $5 in one year. That means you would end up with $505. The more money you put in a savings account, the more interest you will earn. | Presentation notes

Point out that different types of savings accounts offer different interest rates. A basic savings account can be a good starting point. As you save up some money, you can look at other types of accounts that might pay higher interest rates. Make a chart on the board with three columns: Keep Money at Home, Regular Savings Account, High Yield Savings Account. Explain that a High Yield Savings Account is an account that offers a higher rate of interest. Tell students to imagine that they have just graduated from high school. Thanks to working summer jobs and getting money as a graduation gift, they have saved up $500. Write down $500 in each column. Now ask students to imagine they’ve just finished their first year of college. Point at “Keep Money at Home.” Ask students: if you just kept the money in your room, how much will you have after this first year of college? Answer: $500. Then point to “Regular Savings Account.” Tell students this account offers a 1% interest rate. Ask students: if you put your money in that account, how much will you have after this first year of college? Answer: $505. Then point to “High Yield Savings Account.” Tell students this account offers a 5% interest rate. Ask students: if you put your money in this account, how much will you have after this first year of college? Answer: $525. Point out that higher yield accounts may require a bigger opening deposit—in other words, you may need to have a certain amount of money in order to open one. But it can be a good goal to save money in a regular savings account until you get enough to open a high yield account. |

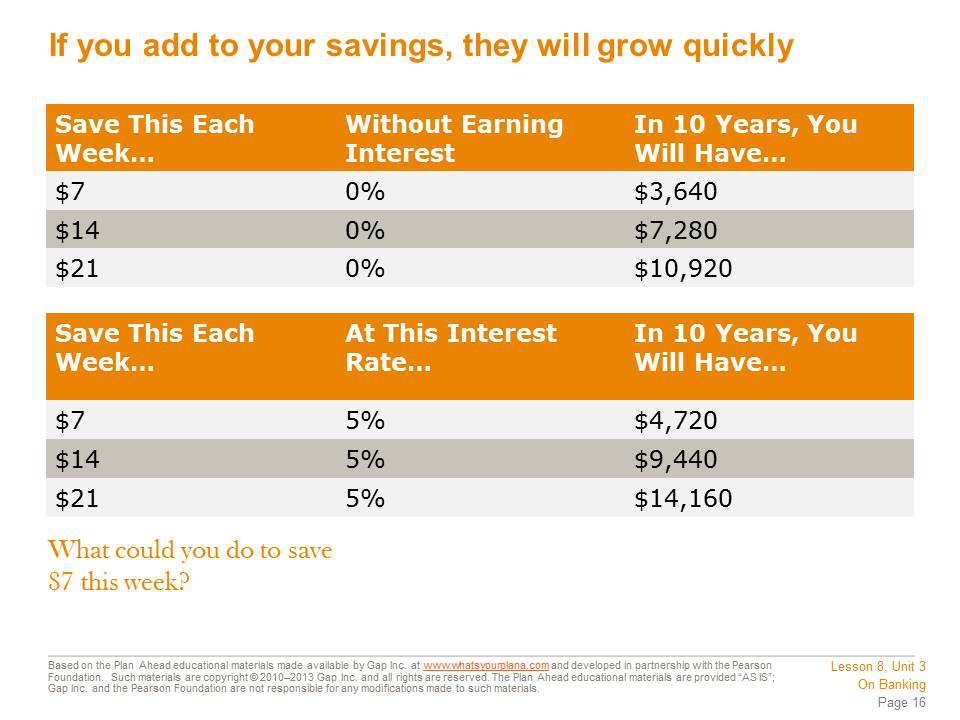

Interest helps your savings add up. Imagine, if you tried to save $7 each week and put it in an account that earned 5% interest, you would end up with $4,720 in 10 years. That’s almost $5,000 you would have, just from that little bit of savings. If you skipped grabbing a latte one morning or ate one meal at home instead of getting fast food, that’s your $7 in savings, right there.

| Presentation notes

Ask students: are you surprised by how much you can save over time? Point out that this is the advantage of saving up over a longer period of time. Sometimes it can be hard to save money right now for something that seems a long way away, like buying a car or paying for college. But if you can get yourself organized enough to save a little bit—even $5 or $10 a week—you can end up with a lot of money over time. Ask students to imagine something they think they would want to spend money on in the next 5 or 10 years—something big that they can’t afford right now. This could be buying a car, paying for school, paying for a wedding, taking a great vacation, or having enough money to move out of their parents’ home. If they started saving just a little bit of money now and put it in a savings account, they could get a lot of money put aside for that future goal. Point out that this is how many adults save up enough money to buy a house or to pay for their retirement—they put aside small amounts of money over time and it builds up.

|

Most major banks now offer online access, which means you can check your account balance, move money between your accounts, or even make payments through the bank’s website. If you are comfortable using the computer, online banking can be very convenient. You don’t need to write checks that you need to send in the mail, and you can check your balance while sitting comfortably at home, listening to your favorite music. Banks are very careful with their online access so your account stays safe and protected. Today there are even “virtual banks” that don’t have any branches at all—you do all of your banking through the Internet, the phone, and ATM machines. | Presentation notes

Ask students to raise their hands if they spend a lot of time online, either on the computer or on their cell phone. Point out that for people who are comfortable with the Internet, online banking or mobile banking (banking on your cell phone) can be a good option. Ask students: can you think of anything to be careful about with online banking? Remind students about some of what they learned about online security during Lesson 6. When they use online banking, students need to be careful to make sure they’re using a reliable website, and they need to be sure not to share their account information or password with anybody. However, if they take those precautions, online banking can be a great way to manage their money.

|

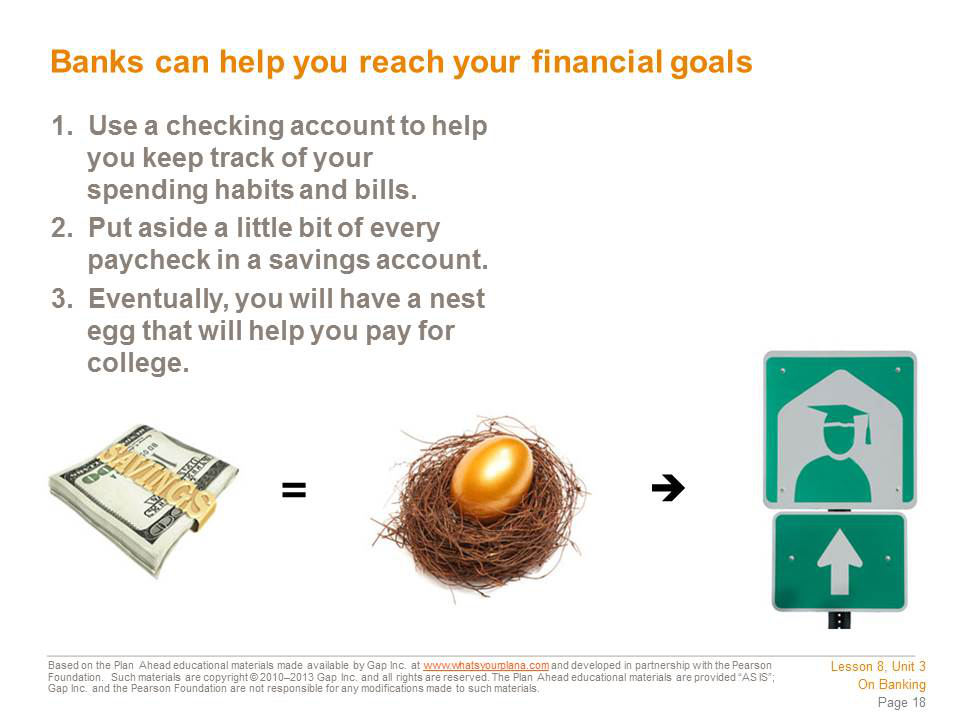

Once you get a job—and this could be part-time, such as babysitting or bagging groceries—opening a savings and checking account is really smart. It’s hard to stay on a budget. If you cash your whole paycheck, you will spend it before you know it and you won’t be sure where the money went. If you deposit your paycheck into your checking account and just let yourself have a little spending money, you will take control of your spending habits. You can start saving up for the future too. A “nest egg” is the money you’ve been saving up for something important. We always think that people are rich because they make a lot of money. But more often, people who are financially successful are good at saving and spending what they have wisely. | Presentation notes

|

Teacher Resource 8.4

Key: Flash Cards on Banking

Use the following key to guide students in the flash card activity. Use the blank cards for terms you want the students to define that have not been included.

| DEFINITIONS (PROVIDED ON FLASH CARDS) | TERMS (STUDENTS FILL IN) |

| A machine that allows you to get access to your bank accounts, even if the bank is closed. | ATM |

| A document the bank sends you every month that lists all of the banking activity that occurred in the previous month, including which checks cleared. | BANK STATEMENT |

| When you write a check but don’t have enough money in your account to cover it. | BOUNCE A CHECK |

| Money lent to people for personal and household use. | CONSUMER CREDIT |

| A card that allows a person to purchase goods and services by paying with borrowed money. | CREDIT CARD |

| An ATM card that also allows a person to purchase goods and services with money from their checking account. | DEBIT CARD |

| To add money to an account, such as when a person makes a deposit. | CREDIT |

| A nonprofit financial institution that is owned by its members. | CREDIT UNION |

| The state of owing more money than you can pay. | DEBT |

| The annual percentage amount you earn in a savings account or have to pay for on a credit card or other credit opportunity. | INTEREST RATE |

| A service banks and credit unions offer that allows customers to manage their money over the Internet instead of going to a branch. | ONLINE BANKING |

| A business that charges an interest to cash a check. | CHECK CASHING BUSINESS |

| A business that advances people money on their upcoming paychecks for a hefty fee. | PAYDAY LOAN STORE |

| A record book a person keeps of all credits and debits to her checking account. | REGISTER |

| The process of taking money out of an account. | WITHDRAWAL |

| To take money out of an account, such as when a person writes a check to pay a bill. | DEBIT |

| When you check your monthly bank statement against what you have recorded in your register. | BALANCE YOUR CHECKBOOK/CHECKING ACCOUNT |

| A service offered by some employers by which paychecks are deposited electronically into the employee’s account. | DIRECT DEPOSIT |

| The Federal Deposit Insurance Corporation; the FDIC insures money in your bank account up to $250,000. | FDIC |

| An interest-bearing account people use to save money, as opposed to paying everyday or monthly expenses. | SAVINGS ACCOUNT |

Teacher Resource 8.5

Test: Banking

Student Name:__________________________________________________Date:___________

Directions: Respond to the questions below in complete sentences.

1. What’s the difference between a bank and a payday loan store or check cashing business?

2. Why are banks safe places to keep your money?

3. Besides writing checks, what’s another way you can pay for things using your checking account?

4. What does it mean when you “bounce” a check? What happens if you bounce a lot of checks?

5. Name two reasons why it is better to put your money in a savings account rather than keep it at home.

6. What is overdraft protection? How does it work?

7. How much money would you earn after one year if you put $500 into a savings account with 1% interest?

8. Name two things you can do through online banking.

9.

On January 17th, Tre does some grocery shopping for his mom. He writes a check for $52.17 to Main Street Market. Fill out the check below.

10. Now, enter the check you just filled out into Tre’s check register below.

Check Number

| Date

| Transaction Description

| Ö

| Payment/Debit

| Deposit/Credit

| Balance

|

| 102 | 1/12 | City Gas & Electric | 76.89 | 80.11 |

| 1/13 | Deposit | 100.00 | 180.11 |

| 1/14 | Tommy’s Restaurant | 13.65 | 166.46 |

| 103 | 1/15 | Sprint | 45.23 | 121.23 |

Teacher Resource 8.6

Answer Key: Test on Banking

While student answers will vary, the following answer key contains the basic knowledge and concepts to be stated in their responses. Use your preferred scoring or point system to assess the tests.

1. What’s the difference between a bank and a payday loan store or check cashing business? You can earn interest at a bank, while payday loan stores and check cashing businesses charge you money.

2. Why are banks safe places to keep your money? They are insured (by the FDIC), and they are confidential.

3. Besides writing checks, what’s another way you can pay for things using your checking account? You can pay for things by using your debit card.

4. What does it mean when you “bounce” a check? What happens if you bounce a lot of checks? You wrote a check, but didn’t have enough money in your account to cover it, so the bank rejects the check. Banks charge a fee for each check you bounce, and if you bounce a lot of checks, you can get in trouble with the law.

5. Name two reasons why it is better to put your money in a savings account rather than keep it at home. You won’t be as tempted to spend it. You will earn interest on it in a savings account.

6. What is overdraft protection? How does it work? Overdraft protection helps you avoid bouncing checks. If you write a check and don’t have the money to cover it, the bank will advance you the money to cover the check. However, once you do have money in your account again, the bank will deduct the amount of the check, and will also charge you a fee.

7. How much money would you earn after one year if you put $500 into a savings account with 1% interest? You would earn $5.

8. Name two things you can do through online banking. You can check your account balance. You can make payments/pay bills. You can transfer funds between accounts. You can read your monthly statement.

9. On January 17th, Tre does some grocery shopping for his mom. He writes a check for $52.17 to Main Street Market. Fill out the check below. Check student’s work for completeness and accuracy.

10. Now, enter the check you just wrote into Tre’s check register below. Check student’s work for completeness and accuracy.

Teacher Resource 8.7

Key Vocabulary: Personal Finance

These are terms to be introduced or reinforced in this lesson.

| Term | Definition |

| ATM | Automated teller machine; a machine that allows you to get access to your bank accounts, even if the bank is closed. |

| bank | An institution where people keep their money. |

| bank statement | A document the bank sends you every month that lists all of the banking activity that occurred in the previous month, including which checks cleared. |

| bounce a check | To have a check rejected for insufficient funds. |

| check | A written order that directs the bank to pay money. |

| checking account | A federally insured service provided by banks and credit unions that allows individuals and businesses to deposit money and withdraw funds. |

| credit union | A nonprofit financial institution that is owned by its members. |

| debit | To take money out of an account, such as when a person writes a check to pay a bill. |

| debit card | An ATM card that can be used to make purchases from a person’s checking account. Looks similar to a credit card and can be used in place of cash or check. |

| debt | A state of owing more money than one can pay. |

| deposit | Money added to a person’s account, such as a paycheck. |

| direct deposit | A service offered by some employers by which paychecks are deposited electronically into the employee’s account. |

| FDIC | The Federal Deposit Insurance Corporation; the FDIC insures money in your bank account up to $250,000. |

| financial literacy | The ability to understand finance and to make informed decisions about money. |

| interest rate | The annual percentage amount you earn in a savings account or have to pay for on a credit card or other credit opportunity. |

| online banking | A service banks and credit unions offer that allows customers to manage their money over the Internet instead of going to a branch. |

| overdraft protection | A service offered by some banks and credit unions for checking accounts to cover a check that would otherwise bounce. Once the customer has the money in his account again, the bank takes the money owed and charges a fee. |

| payday loan store | A business that advances people money on their upcoming paychecks for a hefty fee. |

| PIN | Personal identification number; the customer enters the PIN at the ATM to prove his identity. |

| register | A record a person keeps of all credits and debits to her checking account. |

| savings account | An interest bearing account people use to save money, as opposed to paying for everyday or monthly expenses. |

| withdrawal | The process of taking money out of an account. |

Teacher Resource 8.8

Bibliography: Personal Finance

The following sources were used in the preparation of this lesson and may be useful for your reference or as classroom resources. We check and update the URLs annually to ensure that they continue to be useful.

Covey, Sean. The 6 Most Important Decisions You’ll Ever Make. New York: Fireside, 2006.

Lapan, Richard T. Career Development Across the K-16 Years. Alexandria, VA: American Counseling Association, 2004.

Money Matters: Teen Personal Finance Guide. Charles Schwab Foundation and Boys and Girls Clubs of America, 2004.

Pestalozzi, Tina. Life Skills 101: A Practical Guide to Leaving Home and Living on Your Own. Cortland, OH: Stonewood Publications, 2009.

Online

“Advantages of Online Banking.” MsMoney.com, http://www.msmoney.com/mm/banking/onlinebk/bank_adv.htm (accessed July 11, 2013).

“Budget Worksheet.” About.com: Financial Planning, http://financialplan.about.com/cs/budgeting/l/blbudget.htm (accessed July 11, 2013).

Choi, Laura. “Financial Education in San Francisco: A Study of Local Practitioners, Service Gaps and Promising Practices, November 2009.” Federal Reserve Bank of San Francisco, http://www.frbsf.org/publications/community/wpapers/2009/wp2009-08.pdf (accessed July 11, 2013).

“Compare Utility & Essential Home Services Prices Among Top U.S. Cities: San Francisco.” The WhiteFence Index, http://www.whitefenceindex.com/city/San-Francisco/state/CA (accessed July 11, 2013).

“Consumer Price Index for the San Francisco Area, April 2012.” Bureau of Labor Statistics, http://www.bls.gov/ro9/cpisanf.htm (accessed July 11, 2013).

“Cost of Living Calculator: San Francisco.” PayScale, http://www.payscale.com/cost-of-living-calculator/California-San-Francisco (accessed July 11, 2013).

“Cultural Currency—The Business Journal.” California Capital, April 30, 2004, http://www.cacapital.org/news/cultural_currency.html (accessed July 11, 2013).

“Financial literacy.” Wikipedia, http://en.wikipedia.org/wiki/Financial_literacy (accessed July 11, 2013).

“How Banks Work.” The Mint, http://www.themint.org/teens/how-banks-work.html (accessed July 11, 2013).

“Passes, Tickets and Single-Ride Ticket Booklets.” San Francisco Municipal Transportation Agency, http://www.sfmta.com/cms/mfares/passes.htm#monthly (accessed July 11, 2013).

“Practical Money Skills for Life: Financial Literacy for Everyone.” Practical Money Skills, http://www.practicalmoneyskills.com/ (accessed July 11, 2013).

Said, Carolyn: “Rental Competition Fierce in S.F.’s market” SFGate.com, May 9, 2012, http://www.sfgate.com/cgi-bin/article.cgi?f=/c/a/2012/05/09/BU551OD1PL.DTL&feed=rss.news (accessed July 11, 2013).

Voelcker, John. “Yet Another Reason To Buy a Toyota Prius: Cheap Insurance!” All About Prius, August 18, 2009, http://www.allaboutprius.com/blog/1033929_yet-another-reason-to-buy-a-toyota-prius-cheap-insurance (accessed July 11, 2013).

“What is online banking?” Bankrate, http://www.bankrate.com/brm/olbstep2.asp (accessed July 11, 2013).

Based on the Plan Ahead educational materials made available by Gap Inc. at www.whatsyourplana.com and developed in partnership with the Pearson Foundation. Such materials are copyright © 2010–2013 Gap Inc. and all rights are reserved. The Plan Ahead educational materials are provided “AS IS”; Gap Inc. and the Pearson Foundation are not responsible for any modifications made to such materials.

1